Introduction:

Money is everybody’s need. Since, every single day we purchase one thing or another to meet consumption needs. No one can even imagine spending a day without money. So how money took place and why we prefer money over old system of exchange. These are the things you will know about money in elaboration in this chapter. Let’s begin with the earlier system of exchange.

How was the exchange system in old times?

In old times, people used to exchange goods for goods. This system of exchange was called barter system.

- Barter system has several features:-

- Direct exchange of good and services (without the use of money).

- The need of double coincidence of wants.

Double Coincidence of wants: It means what a person desires to sell is exactly what the other wishes to buy.

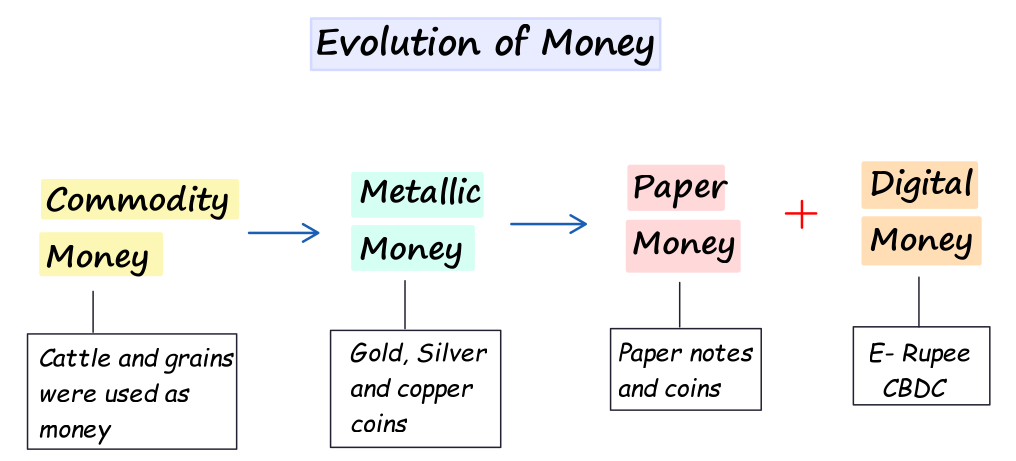

Evolution of Money:

Let’s see how money changed its form over a period of time.

Modern Forms Of Money:

- Modern form of money is currency– paper notes and coins.

- India has its currency called Rupee.

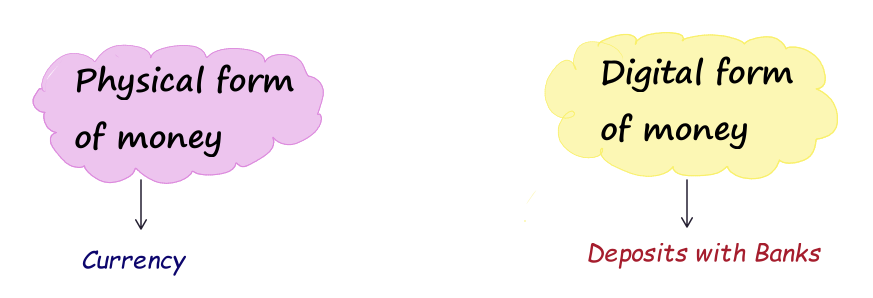

- People can hold money in Physical as well as digital form.

- Features of money:-

- It is a medium of exchange. (plays an intermediate role in exchange process)

- It eliminates the need of double coincidence of wants.

- However, money has no use of its own.

then Why Rupee is widely accepted as a medium of exchange in India?

- It is accepted as a medium of exchange because the currency is authorized by the government of the country.

- Only RBI (Reserve Bank of India) can issue currency on behalf of the central government.

- Moreover, no one can refuse to settle the transaction in Rupee (In India). It is because the law legalizes the use of rupee as a medium of payment.

Note: RBI issues all currency notes except ‘One Rupee’ note. It is because the Government of India’s Ministry of Finance issues one Rupee notes and coins.

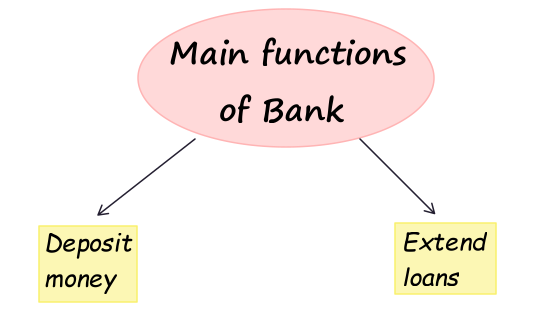

Deposits with Banks:

- Banks are the place where people deposit money (currency).

- Features of banks:

- Bank accepts deposits and keep the money safe.

- It also give interest to the depositors.

- Moreover, Banks provide the facility of demand deposits. It means depositors can demand for withdrawal when need arises.

- Demand Deposits:- When a person withdraws his or her deposited money from the bank on demand, it is called demand deposits.

- The payment on demand deposits can either be made by cheques or cash.

- Cheque: A cheque is a paper instructing the bank to pay a specific amount to the person in whose name the cheque has been issued.

- Benefit: The facility of cheques that banks provide, make it possible to directly settle payments without the use of cash.

- Cheque: A cheque is a paper instructing the bank to pay a specific amount to the person in whose name the cheque has been issued.

- The payment on demand deposits can either be made by cheques or cash.

- But, Banks cannot ask for demand deposits and payments by cheques.

- The modern forms of money- currency and deposits- are closely linked to the working of the modern banking system.

Loan Activities of Banks:

Do this question come to your mind as well that why banks deposit our money? What they do with our deposits? Is there any benefit to them in doing so? or they just do it for social cause? Let’s understand the mechanism of banks better.

- Banks keep only a small proportion of their deposits as cash with themselves. For example, Out of 100% deposits banks just hold 15% as cash. Since they know that not all people will ask for withdrawal at the same time.

- They use major portion of the deposits to extend loans. As people demand loans for various economic activities.

- Banks mediate between those who have surplus funds (depositors) and those who are in need of these funds (the borrowers).

- Banks charge a higher interest rate on loans than what they offer on deposits.

The difference between what is charged from the borrowers and what is paid to depositors is their main source of income.

Two Different Credit Situations:

Before knowing about credit situations, let’s see what is meant by the word credit.

Credit (loans): It refers to an agreement in which the lender supplies the borrower with money, goods or services in return for the promise of future payment.

You must have read about the two stories which shows two credit situations. Therefore, Credit can have different impact in different situation. These credit situations are:

- Credit can play a vital and positive role in helping a person to get better. As it did in the case of Salim.

- Also, it can put the person in risk or push him/her into a debt trap. For instance, Swapna’s case.

Terms of Credit:

In order to take loan, it is must for borrower to agree on the terms and conditions of lender.

- Every loan agreement specifies an interest rate which borrower must pay to the lender along with the repayment of the principal.

- Secondly, lenders may demand for collateral (security) against loans. It reduces the risk of the lender.

- Collateral: It is an asset that the borrower owns (such as land, building, vehicle, livestocks, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid.

- Note: If the borrower fails to repay the loan, the lender has the right to sell the asset or collateral to obtain payment.

- Thirdly, Lender can ask for documentation to verify the borrower’s identity (KYC), ability to repay (income proof/bank statements), loan purpose (invoices), collateral details (title/RC), etc.

- Additionally, lender fixes and communicates how the loan will be repaid (mode of repayment)

- For Example: The borrower and lender agree whether repayment will be through EMIs or a lump sum, along with the frequency, due dates, and payment method (e.g., auto-debit/NACH or cheques). The lender then collects the payments accordingly.

Therefore, Interest rate, collateral and documentation requirement and the mode of repayment together comprise terms of credit.

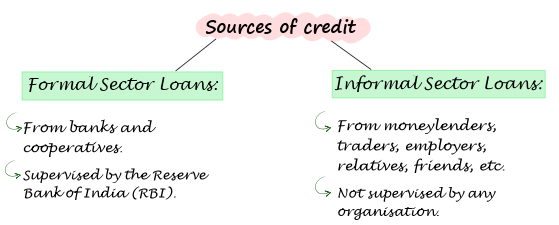

Two Sources of Credit In India:

You learnt about different credit situations and terms of credit. Now let’s talk about the various sources from where people get credit.

| Formal Sector Sources | Informal Sector Sources |

| Banks and cooperatives. | Moneylenders, traders, employers, relatives and friends, etc. |

| The Reserve Bank of India supervises the functioning of formal sources of loans. | There is no organisation which supervises the credit activities of lenders in the informal sector. |

| The formal sector provides loan at lower rate of interest. | Whereas, informal sector charges higher interest rate. |

| These sources use written agreements with disclosed interest and charges. | These sources often use verbal terms with less transparency. |

| Formal lenders use standardised interest, documentation etc. | Informal lenders set their own terms |

- Reserve bank of India : As supervisor of banks

- The RBI monitors the banks in actually maintaining cash balance.

- RBI sees that the banks give loans not just to profit-making but also to small cultivators, small scale industries, to small borrowers etc.

- Periodically, banks have to submit information to the RBI on how much they are lending, to whom, at what interest rate, etc.

Which sector more credit is coming from?

- Among poor/rural households, a large share still comes from the informal sector This is due to various reasons:

- Banks are not present everywhere.

- Bank loans require proper documents and collateral.

- Note: Absence of collateral is one of the major reasons which prevents the poor form getting bank loans.

Why Banks and cooperative societies need to lend more ?

- It is to reduce dependence on informal lenders who charge very high interest.

- Also, to provide cheap and timely credit for farms, self-employed and small businesses.

- Moreover, many rural poor (especially farmers) get trapped into heavy debt. These formal sources can provide loans on more manageable terms.

- Lastly, more lending by bank helps people earn more and get cheap loans for various needs.

- For these reasons, banks and cooperative societies need to lend more, particularly in rural areas.

- It is necessary that everyone receives these formal sector loans.

Why Cheap and affordable credit is crucial?

- Cheap credit helps farmers and small shops buy inputs without much burden of loan.

- People do not have to go to moneylenders who charge very high interest.

- Moreover, cheap credit helps people repay easily and grow their income.

- Affordable credit can encourage people set up their small scale businesses.

- Lastly, the cheap and affordable credit can create new job opportunities and development of the country’s economy.

Self-Help Groups For The Poor:

- Since, poor did not have better access to formal loans, rural people tried out some newer ways of providing loans to the poor.

- The idea was to organize rural poor, in particularly women, into small self help groups and pull (collect) their savings.

Self-Help Groups:

- A typical SHG has 15-20 members, usually belonging to one neighborhood.

- These groups meet and save regularly.

- Saving per member varies from Rs 25 to Rs 100 or more, depending on the ability of the people to save.

- Members can take small loans form the group itself to their needs.

- The group charges very less interest as compare to moneylenders.

- After a year or two, if the group is regular in savings, it becomes eligible for availing loan from the bank.

- Loan is sanctioned in the name of the group and is meant to create self-employment opportunities for the members.

Features Of Self-Help Groups:

- Most of the important decisions regarding the savings and loan activities are taken by the group members.

- The group decides as regards the loans to be granted- the purpose, amount, interest to be charged, repayment schedule etc.

- It is the group which is responsible for the repayment of the loan.

Advantages of SHGs:

- The SHGs help borrowers overcome the problem of lack of collateral.

- They can get timely loans for a variety of purposes and at a reasonable interest rate.

- SHGs help women to become financially self-reliant.

- The regular meetings of the group provide a platform to discuss and act on a variety of social issues such as health, nutrition, domestic violence, etc.

The chapter is now complete! I hope each concept was easy for you to understand and you feel confident about the material. Feel free to share your feedback and comments on the notes posted. Your thoughts are always welcome!

I feel this is one of the most vital info for me. And i’m glad reading your article. However wanna statement on few general things, The site taste is wonderful, the articles is actually nice : D. Good job, cheers

“Thank you, I am happy to hear you feel that way!”

Hello my family member! I want to say that this article is awesome, great written and come with approximately all significant infos. I?¦d like to look extra posts like this .

I’ll right away snatch your rss as I can’t find your email subscription link or newsletter service. Do you’ve any? Kindly let me know in order that I may just subscribe. Thanks.

Really the best handwritten notes 🙏🏻👍🏻 also easy and in simple lang which can be understandable to anyone easily. Thanks for helping.

Your appreciating comment means a lot. Thankyou Sukhman

Thank you♥️

😊

Your notes are helpful to me a lot

Thanks 😊